Long-Term

Disability Plan

Updated June 2019

Introduction

The Texas A&M University System offers a Long-Term Disability plan to protect your

income in case an extended disability prevents you from working.

Your group health pays most of your medical bills if you become seriously ill or injured. But how will you pay

your everyday expenses if you are not able to work for an extended period?

You will continue to be paid as long as you are on sick leave and vacation. Then you may be able to receive

additional days of full pay from the sick leave pool. But, if your sickness or injury is severe, these plans may

stop paying benefits before you can return to work.

To ensure financial security for you and your family during an extended disability, The Texas A&M University

System offers a Long-Term Disability (LTD) plan. It is designed to be a source of income if you are unable to

work due to disability.

This booklet provides a summary of your LTD plan provisions. Most of your questions can be answered by

referring to this booklet.

This booklet does not contain every detail about your plan. All details are included in the contract between The

Texas A&M University System and Cigna. The contract is the final word on all plan provisions. In case of any

discrepancy between this booklet and the contract, the contract will govern.

This booklet is neither a contract of current or future employment nor a guarantee of payment of benefits. The

A&M System reserves the right to change or end the benefits described in this booklet at any time for any

reason.

Clerical or enrollment errors do not obligate the plan to pay benefits. Errors, when discovered, will be corrected

according to the provisions of the plan contract and published procedures of the A&M System.

Table of Contents

Introduction ............................................................................................................................................................. 2

Participation ............................................................................................................................................................ 5

Enrolling in the Plan ........................................................................................................................................... 5

Changing your Coverage .................................................................................................................................... 5

Reduction in Hours ............................................................................................................................................. 5

Leave of Absence ................................................................................................................................................ 5

Coverage Cost ......................................................................................................................................................... 6

Coverage Cost ..................................................................................................................................................... 6

Taxation .............................................................................................................................................................. 6

When You Qualify For Benefits ............................................................................................................................. 7

Disability ............................................................................................................................................................. 7

Physician Care Required ..................................................................................................................................... 7

Proof of Disability............................................................................................................................................... 7

Waiting Period .................................................................................................................................................... 7

Interruption of Disability .................................................................................................................................... 7

Workplace Modification ..................................................................................................................................... 8

When Benefits are not Payable ........................................................................................................................... 8

Pre-Existing Conditions ...................................................................................................................................... 8

How Your Benefit is Calculated ............................................................................................................................. 9

Your Full LTD Benefit ....................................................................................................................................... 9

Lump Sum Payments .......................................................................................................................................... 9

Income that Offsets your LTD Benefit ............................................................................................................... 9

Your Partial LTD Benefit ................................................................................................................................. 10

How LTD Benefits Are Determined ................................................................................................................. 11

Partial Disability Benefits ................................................................................................................................. 11

Income That Does Not Offset Your LTD Benefit ............................................................................................ 12

Catastrophic Disability Benefit ......................................................................................................................... 13

Rehabilitation .................................................................................................................................................... 13

Family Care Expense Benefit ........................................................................................................................... 14

Indexed Earnings .............................................................................................................................................. 14

Cost-of-Living Increases ................................................................................................................................... 14

Social Security Disability Benefits ................................................................................................................... 14

Workers’ Compensation ................................................................................................................................... 14

How Long Benefits Are Paid ................................................................................................................................ 15

Benefits for Physical Disability ........................................................................................................................ 15

Benefits for Mental Disabilities ........................................................................................................................ 15

Proof of Disability............................................................................................................................................. 15

Reducing Benefit Duration............................................................................................................................ 15

Social Security Normal Retirement Age ....................................................................................................... 15

Recovery ........................................................................................................................................................... 15

If You Die ......................................................................................................................................................... 15

If You Refuse Treatment, Rehabilitation, or Accommodation ......................................................................... 16

Applying For Benefits........................................................................................................................................... 17

How to Appeal a Claim..................................................................................................................................... 17

Claim Payments ................................................................................................................................................ 17

Other Benefits ................................................................................................................................................... 18

Subrogation ....................................................................................................................................................... 18

When Coverage Ends ............................................................................................................................................ 19

Extension of Benefits ........................................................................................................................................ 19

Administrative and Privacy Information .............................................................................................................. 20

Plan Name ......................................................................................................................................................... 20

Plan Sponsor ..................................................................................................................................................... 20

Plan Administrator ............................................................................................................................................ 20

Type of Plan ...................................................................................................................................................... 20

Claims Administrator ........................................................................................................................................ 20

Questions and Complaints ................................................................................................................................ 20

Plan Year ........................................................................................................................................................... 21

Employer Identification Number ...................................................................................................................... 21

Agent For Service of Legal Process .................................................................................................................. 21

Future of the Plan .............................................................................................................................................. 21

Participation

All full-time and some part-time

employees are eligible for LTD coverage.

Coverage can begin on your first day of

work. Participation is voluntary.

You are eligible to participate in the LTD plan if:

You work at least 20-hours a week, and

Your appointment is expected to continue

for a term of at least 4½ months, and

You are eligible to participate in the Teacher

Retirement System of Texas (TRS) or

Optional Retirement Program (ORP)

You are also eligible if you are a graduate

student employee who works at least 50%

time for at least 4½ months.

Eligibility for this plan is subject to change by the

A&M System or the Texas Legislature.

Enrolling in the Plan

Your coverage can take effect either on your hire

date or on your state contribution eligibility date

(the first of the month after your 60th day of

employment) if you enroll before, on, or within

seven days of your hire date. If you enroll beyond

the seventh day of your hire date, but during your

first 45 day enrollment period, your coverage will

take effect on your state contribution eligibility

date.

You must be actively at work on the day your

coverage is to begin. If you are not, coverage will

be delayed until the day after you return to work.

This plan limits benefits due to preexisting

conditions during the first 12-months of coverage

(see “section”).

Changing your Coverage

You can enroll in LTD coverage during your first

60-days of employment or during Open Enrollment.

In some cases you may add coverage if you qualify

with a Life Event.

Adding LTD coverage must be consistent with the

change in status. A Life Event includes:

Employee’s marriage or divorce, or death of

employee’s spouse,

Birth, adoption or death of a dependent

child,

Changes in the employee’s, spouse’s or a

dependent child’s employment status that

affects benefit eligibility,

Changes made by a spouse, during his/her

annual enrollment period with another

employer,

The employee, or spouse becoming eligible

or ineligible for Medicare or Medicaid, or

Significant employer-or carrier-initiated

changes in or cancellation of the

employee’s, spouse’s or dependent child’s

coverage.

You can drop coverage with any qualified Life

Event; however, you cannot re-enroll until the

following annual enrollment period.

Reduction in Hours

If your work hours are reduced to between 50% and

99% time, you may keep the same level of benefits

as you had before the reduction. Should you prefer

to have your benefits and premiums reduced,

contact your Human Resources office.

Leave of Absence

If you take a paid leave of absence, your coverage

will continue and premiums will continue to be

deducted from your pay. However, if you take an

unpaid leave, you must make arrangements to

continue your premium payments or to cancel your

coverage. If you continue your coverage, the

coverage amount and premium will be the same as

before your leave. If you decide to discontinue your

LTD coverage, your coverage will be reinstated

without evidence of insurability when you return,

regardless of the plan year. However, the pre-

existing condition exclusion (see “

Pre-Existing

Conditions”) will apply. You have 60-days after

your return to make enrollment changes.

If you discontinue your coverage while on an

unpaid leave under the Family and Medical Leave

Act, your coverage will be reinstated without

evidence of insurability or pre-existing condition

exclusions when you return from leave. However, if

you are within your first year of plan participation,

pre-existing condition exclusions will still apply, as

explained in “Pre-existing Conditions”.

Coverage Cost

You pay the cost for this optional coverage. The cost is based on your pay and whether

you use tobacco products.

Each month, you pay for Long-Term Disability insurance if you choose to buy coverage. If you waive A&M

System health coverage but certify that you have other health insurance, you may apply part of the state

contribution toward your LTD coverage.

If your coverage begins in the middle of a month, you must pay your full premium for the month. You do not

pay premiums while you are disabled (as defined in “Disability”) and receiving benefits. However, the plan has

a 90-day waiting period before it will pay benefits and premiums are due during the 90-day waiting period (See

“Waiting Period”).

Coverage Cost

The cost of your coverage is based on your pay and whether you use tobacco products. You are considered a

tobacco user if you have used any tobacco products in the last three months. This includes chewing tobacco as

well as smoking products. You can change your tobacco-user category at any time.

If your pay increases during the year (other than on September 1), your coverage amount will increase

immediately and your premiums will increase the following September 1.

Taxation

If you pay the full LTD premium, your LTD benefits will not be taxable when you receive them. If you apply

the state contribution to your premium, your benefit will be taxable.

When You Qualify

For Benefits

You pay the cost for this optional

coverage. The cost is based on your pay

and whether you use tobacco products.

In this plan, long-term disability means a disability

that lasts 90 days or longer. If a disability lasts less

than 90 days, you may be eligible for sick leave,

vacation and sick leave pool benefits. Long-term

disability (LTD) benefits can begin after you have

been disabled for 90 days.

Disability

You are considered disabled if you are unable to

perform one or more of the essential duties of your

job due to sickness or injury and you are earning

80% or less of the amount (adjusted for inflation)

you were earning before you became disabled due

to that sickness or injury. This definition of

disability applies during the 90-day waiting period

and the next 60 months of disability.

You are still considered disabled after this period if

you cannot perform one or more of the essential

duties of any gainful occupation for which you are

reasonably qualified by training, education or

experience.

A gainful occupation is one that can be expected to

provide you an income of at least 65% of your pre-

disability income, adjusted for inflation, up to a

maximum of $8,000, within 12 months of your

return to work.

Disability may be caused by pregnancy, injury,

substance abuse or mental or physical illness.

However, benefits for non-organic mental

disabilities will be paid for a maximum of 24

months (see “Benefits for Mental Disability”).

If you work in a rehabilitative job due to a

disability, you will be considered disabled if you

meet the definition of disability described in this

section.

Physician Care Required

No benefit will be paid for any day on which you

are not under the care of a legally licensed

physician.

Proof of Disability

To qualify for benefits, you must provide, at your

expense, proof of your disability from a licensed

physician. The certifying physician may not be you

or your spouse, child, parent, sister or brother.

Cigna may require certification from a licensed

physician approved or selected by Cigna and may

request additional information as well.

After your disability payments begin, you may be

asked to periodically provide evidence of your

continued disability and continuing treatment by a

licensed physician.

Waiting Period

Benefits will begin after you have been disabled for

90 consecutive days. The 90-day waiting period will

begin on the date Cigna determines that your

disability began. During this 90-day period, you

may use sick leave, vacation and, if approved, sick

leave pool to continue your income for as long as

possible.

Interruption of Disability

If your disability ends and then resumes during the

waiting period, the days of disability before and

after the period(s) of no disability will count toward

the 90-day waiting period. The days on which you

were not disabled will not count toward the waiting

period.

For example, if you become disabled and are unable

to work for 40 days, then return to work for 10

days, and again become and remain disabled from

the same cause, you will be able to begin receiving

benefits 100 days after you first became disabled

(90-day waiting period plus the 10 days you

returned to work).

In most cases, recurrent periods of disability are

considered one period if:

they are due to the same or a related cause,

your coverage continued from the date the

first period ended until the second period

began,

the periods are separated by less than six

months of active full-time work during

which you have performed all of the

material duties of any occupation, and

you are not covered by another group long-

term disability plan and entitled to payments

from that plan.

As long as a disability is considered one period,

only one 90-day waiting period must be satisfied.

For example, if you were disabled for a year and

then returned to work for two months and again

became disabled from the same cause, you could

qualify for benefits immediately. However, if you

had returned to work for six months or more, you

would have to wait another 90 days before LTD

payments would begin again.

Workplace Modification

If a covered injury or illness makes it difficult for

you to perform the essential duties of your regular

occupation, the LTD plan may pay the A&M

System up to one times your monthly LTD benefit

to make changes to your worksite to help you return

to work. Modifications must be approved in

advance by Cigna. Cigna may require that you are

examined or evaluated by a health care professional

or vocational or rehabilitation expert of Cigna’s

choice to evaluate the appropriateness of any

proposed modification.

When Benefits are not Payable

You will not be eligible to receive LTD benefits if

your disability is a result of:

a pre-existing condition (see description

below),

declared or undeclared war or any act of

war,

intentionally self-inflicted injuries, or

commission or attempted commission of a

felony or participation in an illegal

occupation.

Pre-Existing Conditions

A pre-existing condition is a sickness or injury for

which you receive medical treatment, consultation,

care or services (including diagnostic measures) or

take prescribed drugs or medicines during the 90

days before your LTD coverage begins.

The plan will not cover any disability caused by,

contributed to by or resulting from a pre-existing

condition unless the disability begins after you have

been covered under the plan for 12 months.

In determining whether a disability is due to a pre-

existing condition, Cigna will credit you for any

time you were insured under the prior plan. If your

disability is due to a pre-existing condition as

described in this plan, but would not have been due

to a pre-existing condition under the prior plan,

Cigna will pay a benefit equal to the lesser of:

The benefit amount under this plan; or

The disability income insurance benefit that

would have been payable to you under the

prior plan.

If your disability would have been due to a pre-

existing condition under the prior plan, it will be

treated as having been caused by a pre-existing

condition under this plan.

How Your Benefit is

Calculated

If you are disabled, you will receive from

the plan and other sources a combined

benefit equal to 65% of your pay. The

maximum benefit from all sources

combined is $8,000 per month.

The long-term disability plan is designed to provide

income to help meet your everyday expenses should

you become disabled. To do this, the plan works

with other benefits you receive to provide 65% of

your annual pre-disability income of up to

$147,692.

Your Full LTD Benefit

If you are disabled and are either unable to work or

able to work but earn less than 20% of your pre-

disability pay, you will receive a full LTD benefit.

To determine your full LTD benefit, other sources

of disability income are considered. Your LTD

benefit together with these other benefits provides

you 65% of your monthly pre-disability pay up to a

maximum benefit from all sources of $8,000 a

month. Regardless of your other benefits, the LTD

plan will pay you at least $100 a month or 10% of

your monthly benefit before reduction for other

benefits, whichever is more.

These other sources of income include benefits

from Social Security, Workers’ Compensation,

association plans, and other government or

company programs for which you qualify. Your

LTD benefit is based on most other sources of

income for which you are eligible whether or not

you apply for them.

If you are eligible for disability payments from any

plan that offsets your LTD benefit (such as Social

Security or Workers’ Compensation) and you do

not begin receiving those payments immediately for

any reason, Cigna reserves the right to estimate the

monthly benefit amount and to reduce your LTD

benefit by the estimated amount payable from the

other plan.

Your LTD benefit is reduced by benefits from TRS

or ORP when you receive payments from these

plans while you are receiving LTD benefits.

Your benefit will be calculated as of the day Cigna

determines you became totally disabled. The pay

used to figure your benefit will be 1/12 of your

annual budgeted pay as of the day you became

disabled, not counting commissions, bonuses,

overtime, longevity or hazardous duty pay, or other

fringe benefits. Any pay increases that become

effective after your disability begins will not be

considered in determining your benefit. If benefits

are payable for less than a month, you will receive

1/30 of the monthly benefit for each day you are

disabled.

Lump Sum Payments

If you receive a lump-sum benefit from another

source, such as Workers’ Compensation, in order to

figure your LTD plan benefit Cigna will prorate that

lump-sum over the period it would normally be paid

or over a period of five years.

If you receive a retroactive payment from another

plan, Cigna will refigure the benefits you have

already received. You must pay Cigna back for

any overpayments you received.

Income that Offsets your LTD Benefit

Any income you start receiving from certain

sources after your disability begins offsets your

LTD benefits. In other words, the plan takes 65% of

your pay, subtracts any amount you receive from

the following sources, and pays you the remaining

amount as LTD benefits.

Your LTD benefit will be offset by any disability

payments you are eligible to receive from:

Social Security disability benefits to which

you or your family may be entitled because

of your disability or any other governmental

law or program that provides disability or

unemployment benefits as a result of your

job, including the Railroad Retirement Act,

Canada Pension Plan, Canada Old Age

Security Act, Quebec Pension Plan or any

such provincial plan

any group LTD plan

A&M System sick leave, sick leave pool,

emergency leave or holidays

temporary benefits under workers’

compensation law, the Jones Act,

occupational disease law or similar laws,

disability benefits from the Veteran’s

Administration or any other foreign or

domestic government agency, including any

increase in the benefit that becomes

effective after you become disabled under

this plan.

Your LTD benefit will be offset by any benefits you

actually receive from the following while receiving

LTD benefits:

any disability benefits from an employer

retirement plan, including TRS or ORP

any retirement benefits from an employer

retirement plan, including TRS or ORP,

unless you immediately transfer the payment

to another IRS-qualified plan to fund future

retirement payments

Social Security retirement benefits for you

or your family, unless you become disabled

after age 70 and are already receiving Social

Security benefits

regular benefits under Workers’

Compensation law, the Jones Act,

occupational disease law or similar laws,

settlements or judgments, minus associated

costs, of a lawsuit that represents or pays

you for your loss of earnings

Your Partial LTD Benefit

During the first two years of a disability that allows

you to continue working and earning from 20% to

80% of your pre-disability pay, your benefit will be

calculated the same way as a full disability benefit.

However, if your LTD benefit (before reduction for

other income benefits) plus your current earnings

total more than 100% of your pre-disability pay,

your LTD benefit will be reduced so that your total

income is no more than the amount you earned

before disability.

After the first 24-months, your LTD benefit will be

refigured to take into consideration the percentage

of your pre-disability pay you are earning. The

formula that will be used is:

pre-disability pay minus earnings during

disability multiplied by 65%

You will receive at least the minimum LTD benefit

each month from the plan while eligible for a partial

benefit. You will no longer be eligible for LTD

benefits if your disability earnings exceed 80% of

your pre-disability income (your pay as of the day

you became disabled, adjusted for inflation) during

the first 60-months of disability. Your benefit

eligibility will also end any time after this period

when your monthly disability earnings are greater

than your monthly partial LTD benefit. You will not

receive an LTD benefit for any month in which

your earnings exceed the limits described below.

For purposes of calculating your partial LTD

benefit, your disability earnings will be the amount

you are actually earning or the amount you could

earn if you were working to your maximum

capacity, whichever is greater. During your first 60-

months of disability, maximum capacity is the most

work you are able to do and is reasonably available

in your regular occupation. After this period,

maximum capacity is based on the most work you

are able to do and is reasonably available in any

gainful occupation for which you are reasonably

qualified by training, education or experience.

If you refuse an offer of employment that is within

your capabilities as described by your physician and

consistent with your education, training and

experience, the amount of pay you were offered will

be used to figure your partial disability benefit. This

applies to an offer of employment from any

employer.

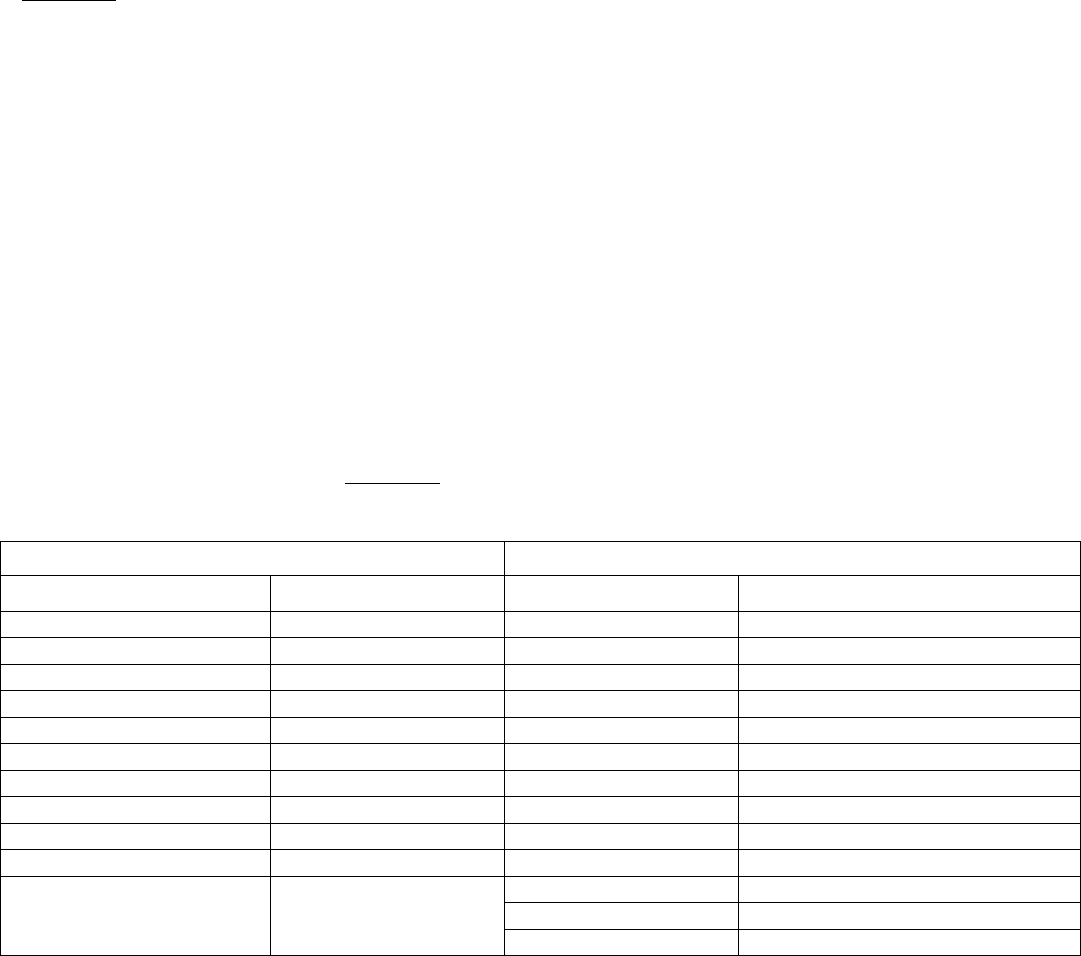

How LTD Benefits Are Determined

Monthly

pay when you became disabled: $2,000

Monthly

pay when you became disabled: $2,500

First the plan figures your full

monthly benefit:

First the plan figures your full monthly benefit:

Monthly pay

$2,000.00

Benefit percentage

x 65%

Target benefit

$1,300.00

Monthly pay

$2,500.00

Benefit percentage

x 65%

Target benefit

$1,625.00

Then the

plan looks at the other benefits you receive:

Then the plan looks at the other benefits you receive:

Soc

ial Security $ 400.00

Workers’

Compensation 200.00

TRS

+ 0.00*

Total other income

$ 600.00

Social Security

$ 600.00**

Workers’

Compensation 600.00

TRS

+ 800.00**

Total other income

$2,000.00

Your LTD benefit i

s your target benefit minus the

other benefits you receive:

Your other income is more than your target benefit.

Therefore, you receive the minimum

benefit -- $100 or

10% of your target benefit.

Target LTD benefit

$1,300.00

Other income benefits

- 600.00

Actual LTD benefit

$ 700.00

Target benefit

$1,625.00

Minimum percentage

x 10%

Minimum benefit

$ 162.50

Your total income during disability is

your

LTD benefit plus the other

benefits you

receive:

Since 10% of your target benefit is more than $100, your

LTD benefit is $162.50. Your total income disability is

your LTD benefit plus the other benefits you receive:

LTD benefit

$ 700.00

Other

income benefits + 600.00

T

otal disability income $1,300.00

LTD benefit

$ 162.50

Other income benefits

+2,000.00

T

otal disability income $2,162.50

*Assumes you elect to defer payment of your benefit until you no longer are receiving LTD payments.

**Assumes you elect to receive TRS benefit while you are receiving LTD benefits. This is taxable income. In

some cases, Social Security benefits and other sources of income could also be taxable.

Partial Disability Benefits

If you continue to work with a disability or take a rehabilitative job and earn 20% to 80% of your pre-

disability pay, here’s how your benefit will be figured. Using the first example on page 12, your pay before

disability was $2,000. Your unreduced disability benefit is $1,300 (65% of $2,000). Since most other

disability income sources do not pay benefits for partial disability, we’ll assume you receive no other

benefits. Assuming you work part time and earn $500 a month, here’s how your disability income will be

figured:

First 24-months

LTD benefit $1,300

plus

Post-disability pay + 500

Total income during

partial disability $1,800

After first 24-months

Pre-disability pay $2,000

minus

Post-disability pay - 500

$1,500

multiplied by x 65%

Partial disability $ 975

Your total disability income in this case is your partial disability

benefit plus your post-disability pay:

Partial LTD benefit $ 975

plus

Post-disability pay + 500

Total income during

partial disability $1,475

Your benefit eligibility will also end any time after this period when your monthly disability earnings are greater

than your monthly partial LTD benefit. You will not receive an LTD benefit for any month in which your

earnings exceed the limits described below.

For purposes of calculating your partial LTD benefit, your disability earnings will be the amount you are

actually earning or the amount you could earn if you were working to your maximum capacity, whichever is

greater. During your first 60-months of disability, maximum capacity is the most work you are able to do and is

reasonably available in your regular occupation. After this period, maximum capacity is based on the most work

you are able to do and is reasonably available in any gainful occupation for which you are reasonably qualified

by training, education or experience.

If you refuse an offer of employment that is within your capabilities as described by your physician and

consistent with your education, training and experience, the amount of pay you were offered will be used to

figure your partial disability benefit. This applies to an offer of employment from any employer.

Income That Does Not Offset Your LTD Benefit

While most group benefits offset—or reduce—the amount you receive from the LTD plan, some sources of

income do not affect your benefit. These include any income you receive from:

A&M System vacation

a no-fault automobile policy

personal investments

personal disability income plan not obtained through a group- or employer-related program

credit disability insurance or franchise disability income plans

Veteran’s Administration disability benefits, if payments began before your disability began

military retirement benefits

profit sharing, employee stock, thrift, 403(b) (excluding ORP or another employer-funded retirement

plan) or 401(k) plans

individual retirement accounts, individual tax-sheltered annuities, tax-deferred accounts, deferred

compensation plans, Keoghs or capital accounts

another employer’s retirement plan, if payments began before your disability began

group voluntary AD&D plans for partial or full paralysis

long-term care plans

Catastrophic Disability Benefit

A “Catastrophic Disability” means you are either

unable to perform, without Substantial Assistance,

at least two Activities of Daily Living, or you have

a severe cognitive impairment that requires

substantial supervision to protect you or others from

threats to health and safety. “Activities of Daily

Living” are:

1. Bathing (i.e., washing oneself in a shower or

tub, including getting into or out of the tub

or shower, or washing oneself by sponge

bath.)

2. Dressing oneself by putting on and taking

off all items of clothing and needed braces,

fasteners and artificial limbs.

3. Continence (i.e., the ability to maintain

control of one’s own bowel and bladder

function; or when un- able to maintain

bowel or bladder function, the ability to

perform associated hygiene, including

caring for a catheter or colostomy bag).

4. Toileting oneself by getting to and from the

toilet, getting on and off the toilet, and

performing personal hygiene associated with

toileting.

5. Feeding oneself by getting nourishment into

one’s own body either from eating food that

is made available to you in a receptacle such

as a plate, cup or table, or by feeding oneself

by a feeding tube or intravenously.

6. Transferring (i.e., the ability to get oneself

into or out of a bed, a chair or wheelchair; or

the ability to move from place to place either

by walking, use of a wheelchair, or some

other means.)

“Cognitive Impairment” means the loss or

deterioration in intellectual capacity that meets

these requirements:

1. The loss or deterioration in intellectual

capacity is comparable to and includes

Alzheimer’s disease and similar forms of

irreversible dementia;

2. The loss or deterioration in intellectual

capacity is measured by clinical evidence

and standardized tests that reliably measure

impairment in the individual’s short-term

and long-term memory, orientation as to

person, place, or time and deductive or

abstract reasoning.

“Substantial Assistance” means the physical

assistance of another person without which you

would not be able to perform an activity of daily

living; or the constant presence of another person

within arm’s reach that is necessary to prevent, by

physical intervention, injury to you while you are

performing an activity of daily living.

“Substantial Supervision” means continual

oversight that may include cueing by verbal

prompting, gestures, or other demonstrations by

another person, and which is needed to protect you

from threats to health and safety.

Catastrophic Disability Benefits are payable when

the Insurer determines that you have a Catastrophic

Disability that is due to the same sickness or injury

for which Disability Benefits are payable under this

Policy. The benefits are payable only while these

conditions are met:

1. You are receiving monthly Disability

Benefits under the Policy.

2. Your Catastrophic Disability lasted at least

through the Elimination Period.

3. You submit satisfactory proof of

Catastrophic Disability to Cigna.

Benefits are payable monthly at a rate equal to 10%

of your monthly covered earnings to a maximum

monthly benefit of $1,333. This benefit is not

reduced by any other source of income. For periods

of less than one month, Cigna will pay 1/30th of the

monthly benefit for catastrophic disability for each

day.

Catastrophic Disability Benefits end on the earliest

of:

1. the date your Catastrophic Disability ends;

2. the date you are no longer receiving monthly

disability benefits under the Policy;

3. the date you fail to submit proof of

continuing Catastrophic Disability; or

4. the date you die.

Rehabilitation

You may receive partial disability benefits as

described above when you participate in a

rehabilitation program. With Cigna’s approval, a

rehabilitation program may include:

vocational testing,

vocational training,

alternative treatment plans such as support

groups, physical therapy, occupational

therapy and speech therapy,

workplace modifications, or

job placement.

Family Care Expense Benefit

If you have expenses for care of a child or other

family member while you are participating in a

rehabilitation program, the cost of that care, up to

$400 per month per child or family member, will be

covered.

Dependent care expenses are those for care of your

children younger than 13 or an older member of

your household who is mentally or physically

disabled and incapable of independent living.

Your dependent care credit cannot be more than

your earnings and cannot be taken for more than 24

months. You must provide receipts from your

caregiver. The caregiver may not be a member of

your family, or living with you.

Indexed Earnings

For the first 12 months that benefits are payable,

your Indexed Earnings equal your covered earnings.

After 12 monthly benefits are paid, your Indexed

Earnings are your covered earnings, plus an

increase applied on each anniversary of the date the

monthly benefits became payable. The amount of

each increase will be the lesser of 10% of your

Indexed Earnings during your preceding year of

disability; or the rate of increase in the Consumer

Price Index (CPI-W) during the preceding calendar

year.

Cost-of-Living Increases

Your benefit will be adjusted on the date the 12th

monthly benefit is payable. Further adjustment will

take effect on each anniversary of the first

adjustment. This increase is made to adjust benefits

for cost-of-living increases. You may receive up to

five cost-of-living increases while you receive

benefits.

Social Security Disability Benefits

You and your dependents may be eligible for Social

Security disability payments if you are totally

disabled. These benefits can begin in the sixth

month of disability if your disability prevents you

from doing any substantial, gainful work and is

expected to last at least 12 months or result in death.

The amount is based on your earnings history. You

and the A&M System share the cost of your Social

Security protection. Because of this, Social Security

disability benefits are included as part of the 65% of

pay you receive while disabled. Your LTD

payments will be calculated based on the initial

family Social Security benefit that you, your spouse

and other dependents are entitled to receive. LTD

benefits are not reduced for future Social Security

benefit increases. If you are eligible to receive

Social Security disability benefits but have not

applied for them, they will still be considered as

part of your disability income. In that case, or if you

do not report your Social Security benefit amount,

an estimated amount will be used to calculate your

LTD benefit. Should the estimated benefit later

prove to be incorrect, your LTD benefit will be

adjusted, and you will receive a payment to correct

any underpayment of your LTD benefit.

Instead of having your benefit reduced by an

estimated Social Security benefit, you may sign an

agreement that you will repay Cigna for any

overpayments once Social Security payments begin.

If you supply satisfactory evidence that you applied

for Social Security disability benefits and your

Social Security claim was denied, your LTD benefit

will be calculated without the Social Security offset.

You may be required to appeal the Social Security

denial of your claim. If you have questions about

Social Security disability benefits, contact your

local Social Security office.

Workers’ Compensation

If you become ill or injured on the job, you may be

eligible for two kinds of Workers’ Compensation

benefits:

• medical benefits related to your disability,

and

disability income benefits to help replace

lost income.

Any disability income benefits you receive from

Workers’ Compensation become part of the 65% of

pay you receive during disability. Your Workers’

Compensation premiums are paid by the A&M

System. Benefits are determined by state law.

How Long Benefits Are Paid

Benefits for physical disabilities are payable for as long as you remain disabled up to age

65. Benefits may be paid beyond age 65 depending on your age when you become

disabled. Benefits for non-organic mental disabilities are limited to 24 months.

LTD benefits are designed to replace part of your income while you are disabled (as defined in section

“Disability”) during your working years. To do this, the plan will pay you benefits after 90 days of disability.

Benefits for Physical Disability

Benefits due to physical disabilities will continue while you are disabled until you recover, die or reach age 65.

However, if you become disabled after reaching age 60, payments may extend past age 65 for the greater of the

Reducing Benefit Duration or the Social Security normal retirement age, as shown below.

Benefits for Mental Disabilities

Benefits for mental disabilities are limited to the term of the disability or 24 months, whichever is less. Mental

illness means any psychological, behavioral or emotional disorder or ailment of the mind, including physical

manifestations of these disorders or ailments. It does not include demonstrable, structural brain damage. If you

are confined to an accredited hospital or institution at the end of the 24 months, you will continue to receive

LTD benefits while you remain confined in a hospital or other place licensed to provide medical care for your

disabling condition.

Proof of Disability

Payments may also end if you do not provide periodic proof of your continued disability or you refuse to be

examined at Cigna’s request (see “Disability

”). Payments also end if you are partially disabled and begin

earning more than 80% of your pre-disability pay, adjusted for inflation.

Reducing Benefit Duration

Social Security Normal Retirement Age

Age at time of disability

Benefit duration

Birthdate

SS normal retirement age

Less than 60

To age 65

1937 or earlier

65

60

60 months

1938

65 + 2 months

61

48 months

1939

65 + 4 months

62

42 months

1940

65 + 6 months

63

36 months

1941

65 + 8 months

64

30 months

1942

65 + 10 months

65

24 months

1943-1954

66

66

21 months

1955

66 + 2 months

67

18 months

1956

66 + 4 months

68

15 months

1957

66 + 6 months

69+

12 months

1958

66 + 8 months

1959

66 + 10 months

1960 & later

67

Recovery

You will be considered recovered if you no longer meet the requirements for disability (see “SECTION”).

If You Die

If you die after being disabled for at least 90 continuous days and you have received at least one monthly LTD

benefit, your survivors will receive a benefit of three times your monthly benefit (before reduction for other in-

come benefits and earnings). This will be paid to your spouse or, if you have no spouse, to your children

younger than 26 who are dependent on you for financial support. If you have no spouse or dependent children

younger than 26 it will be paid to your estate. If your survivors are to receive a benefit after your death, that

benefit will be reduced by any overpayment that had been made to you.

If You Refuse Treatment, Rehabilitation, or Accommodation

Your benefits will stop if you refuse to receive recommended treatment that is generally acknowledged by

physicians to cure, correct or limit the disabling condition. Benefits also will stop if you refuse to participate in

a rehabilitation program or if you refuse to cooperate with or try accommodations designed to allow you to

perform the essential duties of your job during your first 60 months of disability or of any job after 60 months

of disability. This includes:

changes to your worksite or job process to accommodate medical limitations, and

adaptive equipment or devices designed to accommodate your medical limitations.

Applying For

Benefits

You must apply for LTD benefits. If your

claim is denied, you may follow a review

process.

If you have a claim for benefits, you should contact

your Human Resources office within 30 days or as

soon as reasonably possible after your disability

begins. That office will give you the forms you need

to apply for LTD benefits.

You must submit written proof of your disability to

Cigna within 90 days after the end of the waiting

period. If you cannot give proof within this period,

you must give proof as soon as reasonably possible.

However, you may not give proof of claim later

than one year after proof is otherwise required,

unless you are not legally competent.

Proof must include:

• date the disability began,

• the cause of the disability,

• the prognosis of your disability,

• your income (including copies of federal and

state tax returns) and,

• evidence that you are under the care of a

physician

• medical documentation,

• names and addresses of medical

practitioners and facilities you are using or

have used, and

• signed authorization for Cigna to obtain

your medical, employment, financial and

other information.

Cigna also has the right to require, as proof of loss,

your signed statement identifying all other income

benefits and satisfactory proof that you and your

dependents have applied for those benefits that are

available.

Cigna may periodically require further proof that

you continue to be disabled and under a physician’s

care. You must comply with all requests by the due

dates. Cigna, at its expense, may require a physical

examination and may do so more than once. You

must also notify Cigna immediately if you return to

work at any job. Disagreements about benefits are

rare, but should you and the company disagree

about your eligibility for or the amount of your

benefit, you may follow a review process.

How to Appeal a Claim

If your claim for benefits is denied in whole or in

part, Cigna will notify you in writing within 90 days

after your claim form was filed. In special

circumstances, Cigna may need an additional 90

days to give you a decision on your claim, but you

will be notified of the delay and the reason for it.

The written notice of claim denial will give specific

reasons for the denial and reference the specific

plan provisions on which the denial is based. It will

also describe any additional material you must

submit and explain the plan’s claim review

procedures.

Within 60 days of receiving written notice of a

claim denial, you or your authorized representative

may submit a written request for reconsideration to

Cigna. Be sure to state why you believe the claim

should not have been denied and submit any data,

questions or comments you think are appropriate.

You may also review any pertinent plan documents.

Your appeal will be reviewed by the claims

administrator.

A decision on the appeal will be made by Cigna

within 60 days after receipt of your request for

review unless special circumstances require

additional time. In no event will a decision be made

more than 120 days after receipt of your request.

The decision based on the review will be in writing

and will include the specific reasons for the decision

as well as specific references to the appropriate plan

provisions on which the decision is based. This is

the final decision on your claim.

Claim Payments

You will receive monthly benefit payments after

you complete your waiting period. Your first check

will be mailed to you at the end of the month

following your benefit start date. Cigna may, at its

option, pay benefits in advance based on an

estimated duration of your disability. You must

repay any overpayments made in error. In other

words, if you became disabled June 15, you would

complete your 90-day waiting period on September

13. That would be your benefit start date. Your first

check would be mailed to you sometime between

September 13 and October 13. Subsequent checks

would be mailed at approximately one-month

intervals as long as you remain eligible for benefits.

Other Benefits

You should also apply immediately after becoming

disabled for Social Security and any other benefits

for which you might qualify.

Subrogation

If you suffer a disability because of the action or

omission of someone else, you should take legal

action to recover lost wages from that person or

entity. If you are receiving LTD benefits and do not

initiate legal action within a reasonable period,

Cigna may take legal action against the person or

entity to recover the cost of the LTD benefits paid

to you.

When Coverage Ends

Coverage normally ends on the last day of the month in which your employment ends. In

some cases, coverage may be extended.

As long as the plan remains in effect, you may be covered by the plan if you continue to meet the eligibility

requirements. Your coverage will generally end on the earliest of the following dates:

the day this policy ends,

the last day of the period for which you paid the premium,

the last day of the month after you ask that your coverage be dropped,

the last day of the month in which your employment ends or you become ineligible for coverage, or

the day the A&M System stops offering the plan.

Your coverage does not end due to a leave of absence unless you stop paying the premium (see “SECTION”).

Extension of Benefits

If you are disabled and entitled to benefits when this plan ends, you will continue to receive benefits as long as

you remain disabled from the same cause. However, benefits will not be paid for longer than they would have

been paid had the policy remained in effect.

Administrative and Privacy Information

Here are some other facts about the plan you might want to keep handy.

Plan Name

The official name of this plan is The Texas A&M University System Group Long-Term Disability Insurance

Program (more familiar names: the Long-Term Disability Plan or LTD Plan).

Plan Sponsor

Director of Benefits Administration

The Texas A&M University System Moore/Connally Building

301 Tarrow Dr., 5th Floor

College Station, TX 77840

(979) 458-6330

Plan Administrator

The plan administrator is the Director of Risk Management and Benefits Administration. Contact at the address

shown for the Plan Sponsor.

Type of Plan

The Long-Term Disability plan is a group welfare plan providing income replacement benefits. It is a fully-

insured plan funded through employee and, in some cases, employer contributions.

Claims Administrator

LTD plan benefits are insured through a contract with Cigna. Claims are also administered by Cigna.

Cigna

P.O. Box 709015

Dallas, TX 75370-9015

(800) 362-4462

The plan contract governs all plan benefits. You may examine a copy of the contract or obtain a copy for a

copying fee by contacting the Plan Sponsor.

Questions and Complaints

If you have a question or a complaint, call Cigna at 1 (800) 362-4462 or write to:

Cigna

P.O. Box 709015

Dallas, TX 75370-9015

If your problem is not resolved, call or write to:

The Texas Department of Insurance

P.O. Box 149104

Austin, TX 78714-9104

Phone: 1 (800) 252-3439 Fax: 1 (512) 475-1771

POLICY NUMBER

VDT98005

Plan Year

Plan records are kept on a plan-year basis. The plan year begins each September 1 and runs through the next

August 31.

Employer Identification Number

74-2648747

Agent For Service of Legal Process

Plan Administrator

Future of the Plan

While The Texas A&M University System intends to continue this plan indefinitely, it may change, suspend or

end the plan at any time for any reason.

If the Long-Term Disability plan ended, benefits would be paid only for disabilities that occurred before the

plan ended. No benefits would be payable for disabilities that occurred after the date the plan ended.

System Benefits Administration

Moore/Connally Building

The Texas A&M University System

301 Tarrow Dr., 5th Floor

College Station, TX 77840